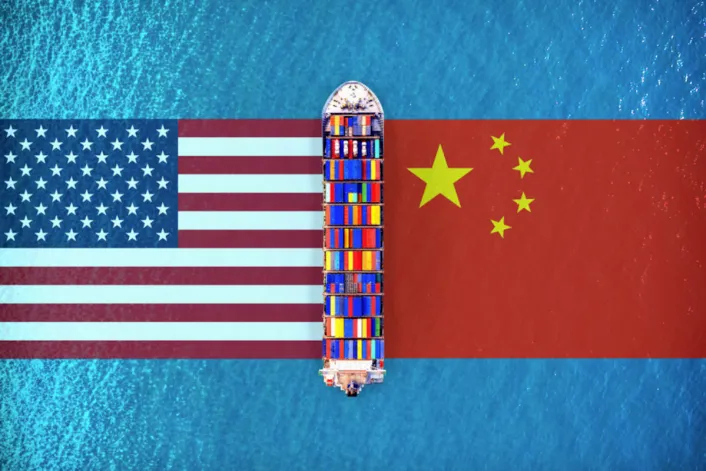

A US Supreme Court ruling, a presidential tantrum, and a frozen European trade deal — all in 72 hours. That was the state of the global trading system as the week began, and if you’re a freight operator in Singapore, an auto-parts maker in Mexico, or a wheat farmer in Kansas, the chaos is not abstract. It’s the price of doing business in 2026, when the world’s two largest economies are exporting incompatible visions of how trade should work — and everyone else is left to pick up the pieces.

On Friday, February 20, the US Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that President Donald Trump had wrongfully invoked the International Emergency Economic Powers Act (IEEPA) to impose his sweeping “reciprocal” tariffs. By that evening, Trump had signed a proclamation imposing a new 10% global tariff under Section 122 of the Trade Act of 1974. By Saturday, February 21, he announced via social media that he was raising it to 15%—the statutory maximum. The speed was breathtaking. So was the legal whiplash: one statute struck down, another invoked within hours, and a rate increase tacked on the next morning via a social media post.+4

The Fallout Hits Europe First

The European Union froze ratification of its US trade deal — the so-called Turnberry Agreement, signed in Scotland last July — until Trump solidifies his upended tariff plans. EU lawmakers on Monday, February 23, suspended legislative work, days after the Supreme Court ruling. Following an emergency meeting in Brussels, lawmakers said the US side of the deal is now “so uncertain” that “nobody knows what will happen”.+1

The Turnberry deal was supposed to bring stability. Signed in July 2025, the agreement committed the EU to a permanent 15% tariff on its exports to the US and approximately $600 billion in American investments and LNG purchases. But an EU assessment found that Trump’s new tariff policy—specifically the Section 122 surcharge which “stacks” on top of existing duties—could push cumulative levies on some of the bloc’s exports as high as 30%. European Parliament trade committee chairman Bernd Lange called it “pure tariff chaos”.+2

The ripple effects are widening. Trade negotiators from India have canceled a planned trip to Washington. It’s believed that Chinese President Xi Jinping may seek to renegotiate during Trump’s scheduled visit to Beijing on March 31, as the court’s decision has given Beijing some leverage.

China’s Record Surplus and the Stability Myth

While Washington generates legal confusion, Beijing projects composure. China’s exports for 2025 grew 5.5% while imports stayed flat, pushing the trade surplus to a record $1.19 trillion — up 20% from 2024. Factories escaped Trump’s tariffs by making deeper inroads into markets beyond the US; shipments to Southeast Asia and Europe surged to offset the tariff-driven slump in US sales.+1

That performance gives Beijing confidence — and ammunition. Chinese officials frame their economy as the reliable partner in a world of American unpredictability. But the stability narrative has limits. Exports accounted for a third of China’s economic growth in 2025 — the highest share since 1997 — while imports were virtually flat, reflecting weak domestic demand. IMF Managing Director Kristalina Georgieva warned that “China is simply too big to generate much growth from exports”.

The numbers tell the story of an economy running on one engine. China has struggled to shake off deflationary pressure as a deepening real estate collapse weighs on household demand. The Rhodium Group warned the record surplus could prompt more protectionist pushback globally, complicating Beijing’s growth targets for 2026.

Southeast Asia: Collateral Beneficiary, Collateral Risk

For the nations wedged between these two giants, the calculus is brutally practical. Rather than reduce US dependence on Asian manufacturing, tariffs have simply rearranged supply chains. Vietnam’s US trade deficit rose more than $20 billion to $145.7 billion in 2025 despite a 20% tariff. Analysts note a fundamental reconfiguration: ASEAN is importing more machinery and intermediate goods from China to produce the exports sent to the US.

That reconfiguration is real, but fragile. The Lowy Institute notes that the new US tariff regime is likely to accelerate ASEAN’s trade diversification strategy, though Cambodia, Vietnam, and Thailand are particularly exposed given their high export reliance on the US market. The World Trade Organization (WTO) has slashed its global merchandise trade volume growth forecast for 2026 to just 0.5%, down from an earlier 1.8%, as tariff impacts ripple through economies.

The practical lesson for third countries is clear: the choice is not between Washington and Beijing but between volatility and dependency. American policy risk — where today’s tariff is tomorrow’s bargaining chip, reshaped by courts and campaign politics — runs parallel to Chinese structure risk, where stable terms can quietly lock partners into relationships that become difficult to rebalance. The new Section 122 tariff applies to roughly $1.2 trillion worth of imports and expires after 150 days on July 24, 2026, unless extended by Congress, injecting yet another countdown into a system already running on temporary fixes.

For supply-chain managers from Jakarta to Frankfurt, the playbook is less about choosing sides than building buffers: diversified suppliers, traceable compliance systems, regional trade agreements that function when the big powers don’t, and the infrastructure — faster customs, interoperable digital systems, accessible trade finance — that keeps goods moving when politics tries to stop them. In a world where trade policy behaves more like weather than architecture, the winners will be those who packed an umbrella.

Original analysis inspired by Y Tony Yang from Asia Times. Additional research and verification conducted through multiple sources.